Decoding Your GRB Statement: A Foreign Service Guide to Federal Total Compensation Part 1 of 2

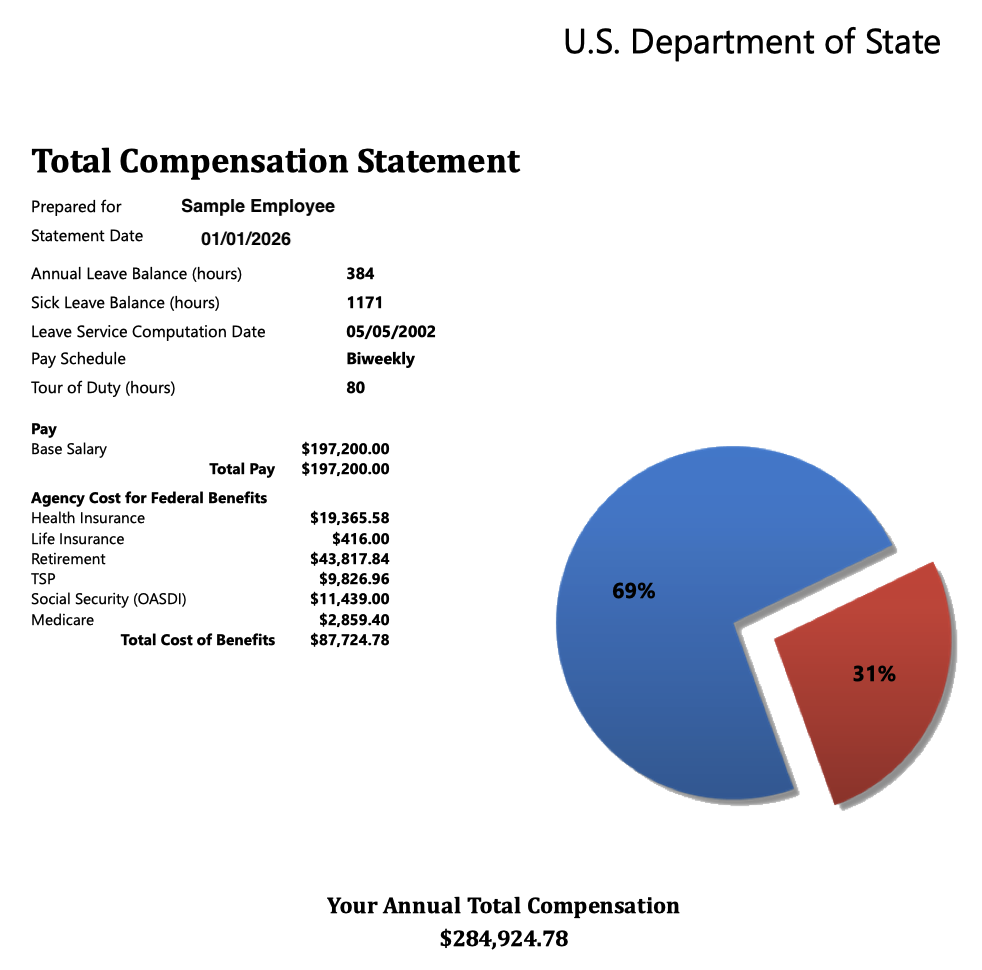

Most Foreign Service employees see their Total Compensation Statement once a year, glance at the pie chart, and move on. The blue slice — base salary — is the part everyone understands. The red slice, labeled "Agency Cost for Federal Benefits," is where things get fuzzy. On a sample statement I've been reviewing recently, that red slice came to $87,724 against a base salary of $197,200. Thirty-one percent of an employee's total compensation is not pocket change, and yet most Foreign Service employees couldn't tell you what's actually in it, much less why each piece is there or how to think about its value.

This post walks through the red slice, line by line. The next post in this series takes a closer look at the single largest item on it — the Foreign Service Pension System (FSPS) employer contribution — which on the statement in front of me runs over $43,000 a year, more than half of the entire red slice on its own.

The red slice, decoded

The agency cost of benefits is a useful number to take seriously, but it groups together things that are quite different in nature. Some entries are genuine employer-paid benefits an employee couldn't replicate on the open market for the same price — health insurance under FEHB and the FSPS pension are the clearest examples. Others are mandatory employment taxes the agency is required to pay on the employee's wages — the employer side of Social Security and Medicare. A few are modest contributions to programs the employee largely funds themselves — FEGLI Basic life insurance is the main example. Lumping these together tends to obscure what's worth a lot, what's worth a little, and what's worth thinking carefully about.

Retirement: the FSPS agency contribution

This is the largest item on the chart — $43,817.84 on the sample statement, more than half of the entire red slice on its own. It represents the agency's actuarially-determined share of funding the future FSPS pension benefit that the employee will eventually receive. Because the pension is the most consequential benefit on the chart, the most often misunderstood, and the area where good planning can have the largest impact across a career, it gets its own treatment in the next post in this series. For this post, we'll just note its scale and move on.

Health insurance (FEHB)

On the sample statement, the agency share of the Foreign Service Benefit Plan (FSBP) High Option Self & Family premium is $744.83 per pay period, or $19,366 a year. The employee pays an additional $248.27 per pay period out of their own paycheck. Federal law caps the agency share of FEHB premiums at 75% of total cost, and FSBP — which is an FEHB plan despite its name — works the same way.

Two points worth understanding here. First, the agency contribution is the same in pre-tax dollars as it is in cash terms, but the employee's $248.27 share is also paid pre-tax through "premium conversion," which is automatic unless the employee affirmatively waives it. Second, and more importantly, FEHB coverage continues into retirement under the same agency-share arrangement, provided the employee has been continuously enrolled in FEHB for the five years immediately before retirement. That continuation feature is one of the most valuable retiree benefits in federal employment. For most federal retirees, the lifetime value of subsidized FEHB rivals the value of a substantial portion of their pension.

TSP: the agency match

The agency contributes up to 5% of base salary to the employee's TSP account each year — 1% automatically (regardless of whether the employee contributes anything), and up to an additional 4% matched against the employee's first 5% of contributions. On the sample statement, the agency TSP contribution shows as $9,826.96, which works out to almost exactly 5% of base salary, confirming the employee is contributing at least 5% themselves to capture the full match.

The single biggest mistake federal employees make with TSP is not contributing at least 5%. Anything less leaves agency match on the table — a direct, immediate, dollar-for-dollar reduction in total compensation that the GRB statement won't flag for you. It also bears mentioning that the agency contribution is always treated as a Traditional (pre-tax) contribution regardless of whether the employee's own contributions are Traditional or Roth. So an employee who contributes exclusively to Roth TSP still accumulates a Traditional balance over time, simply from the match.

Social Security (OASDI), employer share

This line shows $11,439 on the sample statement — the maximum employer-side Social Security tax for 2026, because the employee's base salary exceeds the wage base. For 2026, the Social Security taxable maximum is $184,500, and the OASDI tax rate is 6.2% on both the employee and employer side. Past that wage base, no additional Social Security tax is owed by either party.

Strictly speaking, this entry isn't a "benefit" in the conventional sense — it's a mandatory employment tax. The employee is also paying the same amount on their own side ($11,439 in this case), which doesn't appear on the GRB statement at all. Whether to think of the employer share as part of your compensation is a matter of economic perspective; most economists would say the employer share is effectively absorbed by the employee in the form of suppressed wages, but the federal government separately discloses it on the GRB. Either way, FSPS-covered employees do earn Social Security credit during their federal service, and Social Security is the third leg of the FSPS retirement stool.

Medicare (HI), employer share

$2,859.40 on this statement — 1.45% of base salary with no wage cap. Like the Social Security employer share, this is a mandatory tax rather than a discretionary benefit. It funds the Medicare Part A hospital insurance trust fund.

Worth saying clearly: this is not Part B, which is a separate program an employee pays for individually starting at age 65 if they choose to enroll. The decision of whether to add Part B alongside FEHB in retirement is one of the more nuanced choices in federal retirement planning, and it's a decision the GRB statement doesn't help you with one way or the other.

Life insurance (FEGLI Basic)

$416 a year, the smallest item on the chart. This is the agency's one-third share of the Basic FEGLI premium; the employee pays the other two-thirds. Any FEGLI Option A, B, or C coverage the employee elects is paid entirely by the employee, with no agency match. On the sample statement, the employee carries Option B with three multiples — an additional $594,000 of coverage — for which the agency contributes nothing.

Two practical observations. Basic FEGLI provides coverage equal to the employee's annual rate of basic pay rounded up to the next $1,000 plus $2,000, which on this statement comes to $200,000 of coverage. For many mid-to-late-career Foreign Service employees with families, that's not enough on its own. And FEGLI Option B premiums rise sharply with age — many employees in their late forties and beyond can find cheaper term coverage in the private market on a premium-only basis, particularly if they're in good health.

There is, however, one feature of FEGLI that genuinely has no counterpart in the private term market, and it matters more for Foreign Service employees than for almost any other federal workforce: FEGLI pays out for any cause of death, anywhere in the world. There are no war exclusions, no terrorism exclusions, no high-risk-country carve-outs. Nearly every private term policy carries one or more of these — and they happen to be precisely the perils a Foreign Service employee at a high-threat post is exposed to. An attractive-looking private term quote can become worthless at the moment it's needed most if the exclusion language voids the policy in the very environment the employee is being asked to serve. For employees serving or expecting to serve in dangerous environments, FEGLI's universal coverage is a genuine and uncommon benefit, and worth weighing carefully against any private alternative that looks cheaper on premium alone. FEGLI is convenient. It's not always the cheapest. But on the scope of what it actually covers, it stands alone.

What's not in the red slice

A few things worth knowing aren't on the GRB statement at all but should be part of how you think about your total compensation. Annual leave accrual and the unused-leave lump-sum payment at separation are real compensation that doesn't appear here. Training and FSI courses, which can run into the tens of thousands of dollars for a Foreign Service employee over a career, are not on the chart. Neither are housing, hardship and danger pay differentials, COLA on overseas posts, or education allowances for school-age children — none of which are part of base salary, but all of which are real compensation that's structurally part of a Foreign Service career and largely tax-advantaged when earned abroad. And as I'll discuss in the next post, even the pension itself is worth meaningfully more than the normal-cost contribution shown on the chart suggests. The GRB statement is useful, but it's not the whole picture.

What this means for planning

Three things tend to fall out of an honest look at the GRB statement, leaving aside the pension question we'll take up in the next post.

The first is that the TSP match is real compensation that's invisible to many employees because it accumulates inside their TSP account rather than appearing in their paycheck. Any employee contributing less than 5% of salary is leaving money on the table. The match is funded by the agency contribution shown in the red slice, and capturing it fully should be a baseline expectation, not a stretch goal.

The second is that FEHB and the right to carry it into retirement is, dollar for dollar over a retirement lifetime, one of the most valuable benefits in federal employment, full stop. Five years of continuous enrollment before retirement is the price of admission. For employees considering a mid-career departure or a switch out of federal service, the loss of FEHB continuation is often the most overlooked cost.

The third is that FEGLI Basic — the smallest line on the chart — punches well above its weight for any Foreign Service employee with a high-threat post in their future. The universal coverage feature is something you genuinely cannot replicate in the private term market at any price. Before downgrading FEGLI in favor of cheaper private term, it's worth thinking carefully about what kinds of postings lie ahead.

That brings us to the largest piece of the red slice, the pension, which deserves a closer look than a GRB tour can give it. The next post in this series picks up there, comparing FSPS to FERS and showing what those formulas actually mean in dollars across a Foreign Service career.

William Carrington, CFP®, RMA®, is the founder of Carrington Financial Planning LLC, a virtual fee-only firm serving U.S. Foreign Service families and other federal employees.