FERS, FSPS, and the 1.7% Multiplier: Your Federal Pension Explained Part 2 of 2

In the first post in this series, we walked through the red slice of the GRB Total Compensation Statement — the agency cost of federal benefits — and set aside one piece for closer treatment: the agency's contribution to the Foreign Service Pension System (FSPS). On the sample statement we worked from, that line was $43,817.84, or about 22.2% of base salary. It's the largest item on the chart, more than half of the entire red slice on its own, and the benefit it funds — the pension — is the most consequential element of total compensation in any career Foreign Service household.

This post takes that pension seriously. It explains what the 22.2% agency contribution actually funds, compares the FSPS formula to the standard and enhanced versions of FERS that cover most other federal employees, and shows what those formulas mean in dollars across a realistic Foreign Service career.

What that 22.2% actually represents

The agency contribution to FSPS is the actuarial "normal cost" of the pension: roughly the amount that needs to be set aside today, alongside the employee's own contribution, to fund the future defined benefit the employee will eventually receive. The agency rate is not fixed by statute. Per the Foreign Affairs Manual (3 FAM 6111), it's recalculated periodically to reflect the actuarial cost of delivering FSPS.

To put that 22.2% in perspective: the equivalent agency contribution under regular FERS runs meaningfully lower, because the FERS benefit formula is less generous. The richer FSPS multiplier — 1.7% on the first 20 years versus 1.0% under FERS — costs more to fund, and that cost shows up directly in the red slice of the total compensation pie chart. In a real sense, the size of this line is a quiet measure of how valuable your pension is. The actuaries doing the math know what FSPS will eventually pay out. The 22.2% reflects what it takes to deliver on that promise.

The same three-legged stool

For Foreign Service employees, the pension is one of the most valuable elements of total compensation — and one of the least understood, partly because you're in a different system than the rest of the federal civilian workforce. Across the dining table from a sibling in Civil Service or a spouse working at post, the formulas, the multipliers, and even the words used to describe them can sound similar enough to seem identical when they aren't.

The two systems most relevant to a State Department household are FSPS, which covers Foreign Service employees hired after 1986, and the Federal Employees Retirement System (FERS), which covers Civil Service employees, most Eligible Family Members (EFMs) working at post, and the vast majority of the federal workforce. Both rest on the same retirement architecture: a defined-benefit pension, the Thrift Savings Plan (TSP), and Social Security. Employee contribution rates to the pension are nearly identical. TSP works the same way in both systems, including the agency match. Social Security is Social Security. The structural difference is almost entirely in the pension formula — and to a lesser but still meaningful extent, in the eligibility rules around when you can collect that pension.

The FERS formula

Under FERS, your annual pension at retirement is calculated as one percent of your high-3 average salary, multiplied by your years of creditable service. Your high-3 is the average of the three highest consecutive years of base salary in your career, which for almost everyone means the final three years. Creditable service is most of your federal employment, plus military service if you've made the required deposit, minus any periods for which you withdrew contributions and didn't redeposit.

There is one important enhancement built into FERS. If you retire at age 62 or later and you have at least 20 years of creditable service, the multiplier rises from 1.0% to 1.1%. This is sometimes called the "20/62 rule," and it's a place where careful reading matters. Both conditions are required. A 60-year-old retiring with 25 years of service gets 1.0%. A 62-year-old retiring with 18 years of service gets 1.0%. Only an employee who meets both thresholds at the moment of retirement triggers the 1.1% multiplier, and when they do, that higher rate applies to every year of service — not just the years after 20.

The FSPS formula

FSPS uses a tiered formula that's richer in the first 20 years of service: 1.7% of high-3 for each of your first 20 years, and 1.0% for each year after that. So at 20 years, a Foreign Service employee has earned a pension equal to 34% of high-3. At 25 years, it's 39%. At 30 years, it's 44%. Unlike FERS, there's no age requirement to access the higher multiplier. Whether you retire on an immediate annuity at 50 or are pushed out at mandatory retirement at 65, your first 20 years accrue at 1.7%.

What this looks like in dollars

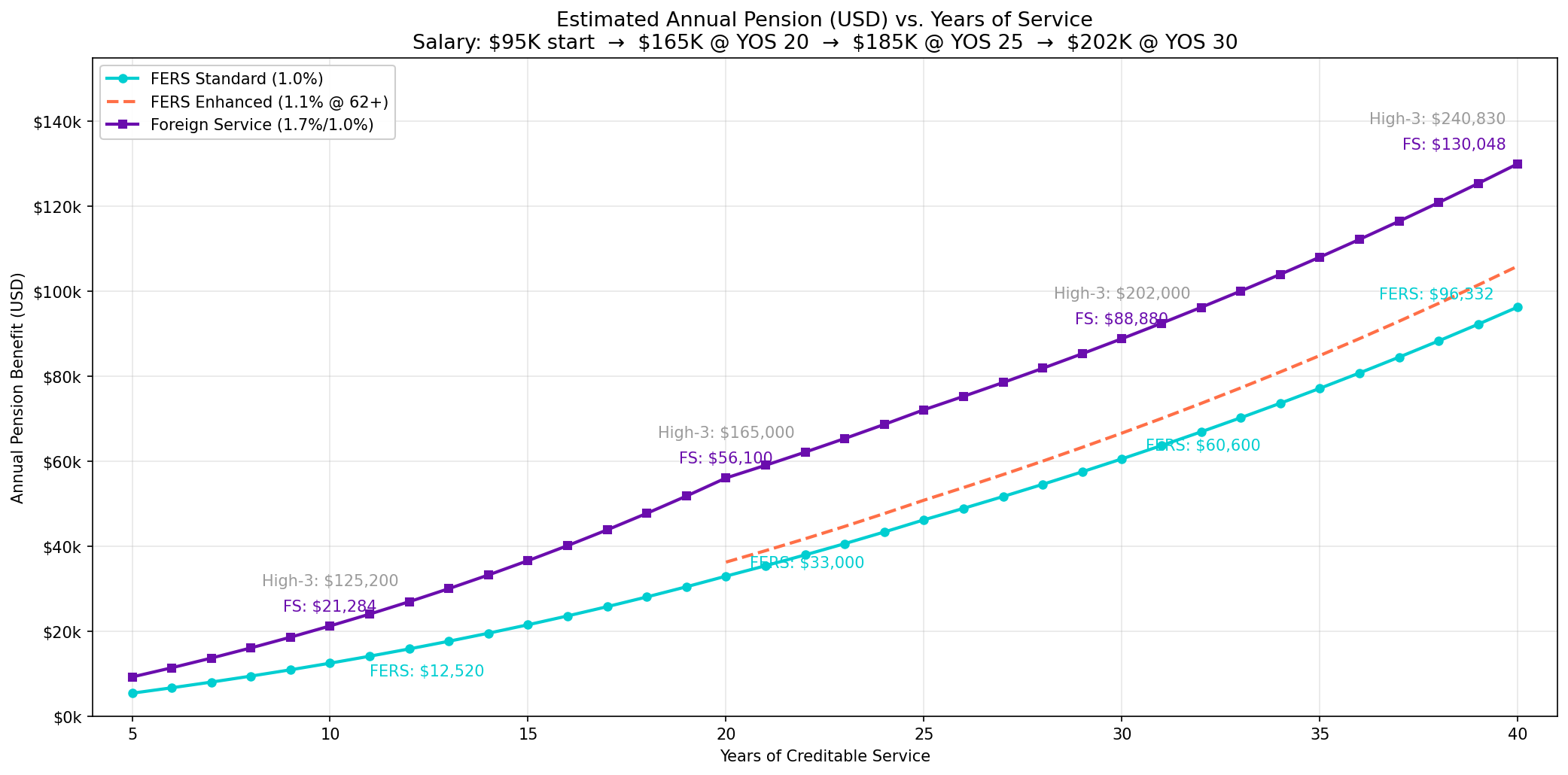

The fairest way to compare the two systems is to put them on the same salary curve. Here, I've modeled a Foreign Service salary trajectory that begins at about $95,000 at year zero and rises to roughly $202,000 by year 30 — a realistic path for a Foreign Service employee who promotes through the senior ranks. The growth tapers as it should, faster in the early-career years when promotions through FS-04 through FS-02 are routine, and slower in the senior grades where movement is harder-earned.

The story the chart tells is most clear at the milestones. At 20 years, FSPS pays $56,100 a year. Enhanced FERS — the dashed orange line, available only if the employee actually works to age 62 — would pay $36,300 for the same career. That's a $19,800 annual gap, and it persists or widens across every later milestone. At 30 years, FSPS reaches $88,880 while enhanced FERS pays $66,660, a gap of $22,220.

The comparison to standard FERS, the solid cyan line, matters at least as much. Most Foreign Service employees don't retire at 62 or later. Many take immediate annuities in their early to mid-fifties under FSPS's more generous eligibility rules. For a Foreign Service career captured at the same 30-year mark, FSPS pays roughly $28,000 a year more than standard FERS would have for the same service and the same high-3. Over a 25-year retirement, undiscounted and before cost-of-living adjustments, that's nearly $700,000 of additional lifetime income.

The same picture in percentages

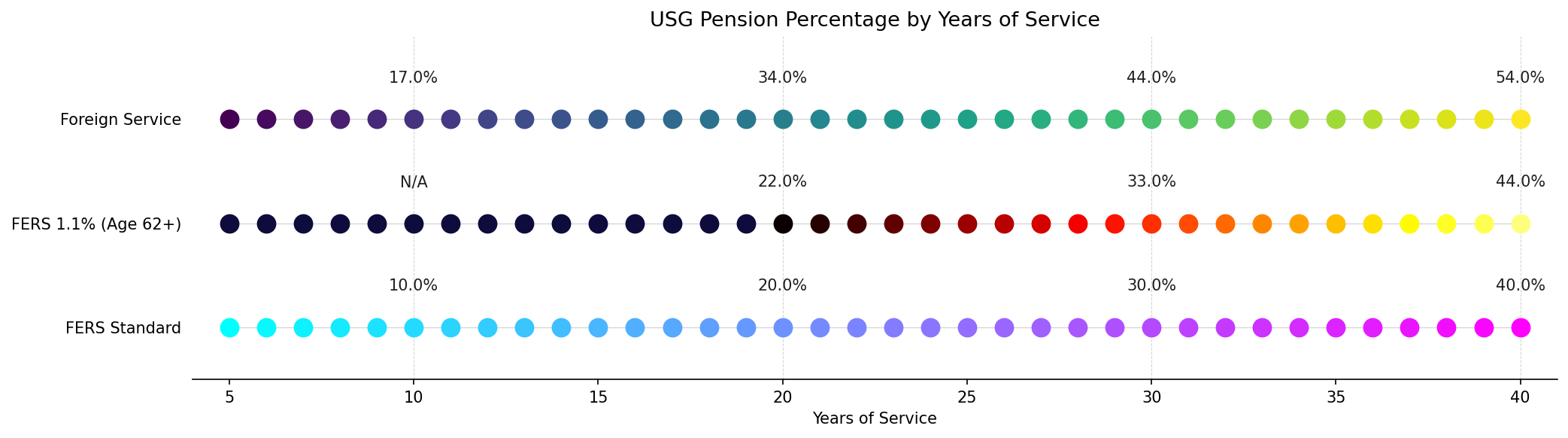

Dollar comparisons depend on the salary path you assume. For households with both a Foreign Service employee and a spouse covered under a different system — which is most State Department households — or for clients who've moved between systems during their careers, the cleaner comparison is the percentage of high-3 that each year of service buys you:

A few things to notice. The Foreign Service line widens its advantage steeply over the first 20 years — that's the 1.7% multiplier doing its work, and it's the period during which FSPS most decisively outperforms either flavor of FERS. The FERS 1.1% line doesn't exist below 20 years of service because the 20/62 rule requires both conditions, so anyone separating before that threshold is firmly on the 1.0% line. And the gap between the top and bottom rows is the practical reality for an EFM spouse retiring alongside their Foreign Service partner: even at 30 years of service, an EFM under standard FERS earns 30% of high-3, while their Foreign Service spouse earns 44%.

Beyond the formula

Two important differences don't show up in either chart, and both matter for planning.

The first is mandatory retirement. FSPS requires separation by age 65, with limited exceptions. FERS Regular has no mandatory retirement age. That cuts both ways: FERS Regular employees can keep accruing service past 65, but they don't have access to the early-retirement provisions that FSPS employees do. FSPS allows immediate retirement at age 50 with 20 years of service, or at any age with 25 years. FERS Regular typically requires reaching the Minimum Retirement Age (57 for most current employees) with 30 years, or age 60 with 20. The threshold for collecting an immediate annuity is a decade lower under FSPS than under most FERS retirement paths.

The second is the Special Retirement Supplement (Annuity Supplement). Both systems pay a bridge benefit from retirement to age 62, designed to approximate the Social Security you can't yet claim. For FSPS, the supplement is available essentially any time you take an immediate annuity, including the early-fifties retirements common in the Foreign Service. For FERS Regular, the supplement is available only when you retire at MRA with 30 years, or at age 60 with 20 — and there's an earnings test that can reduce or eliminate it if you work in retirement.

What this means for planning

The annual normal-cost contribution shown on the GRB report (Total Compensation Statement) understates the value of the FSPS pension. The cost to fund a benefit and the value of the benefit to its recipient are different numbers, and in the case of a defined-benefit pension paid as a lifetime annuity with cost-of-living adjustments and survivor protections, the gap is significant. A 30-year FSPS pension of $88,880 a year, indexed for inflation and protected for a spouse, has a present value that runs into the low millions on standard actuarial assumptions. That value is what good Foreign Service retirement planning is built around.

For an EFM spouse working in a FERS-covered role, the pension math is structurally different from their Foreign Service partner's, and the 1.1% enhancement is unlikely to apply unless they work until 62. Most EFM federal careers end when the Foreign Service employee retires, often in the mid-fifties — well short of the 20/62 threshold. Modeling those careers under standard FERS, with no enhanced multiplier and no immediate supplement, is almost always the right baseline.

For Foreign Service employees themselves, the headline of FSPS isn't really the 1.7% multiplier. It's the flexibility the whole system grants: the ability to retire on an immediate annuity in your early fifties with a substantial pension and a Social Security bridge that doesn't penalize you for working afterward. That flexibility is worth modeling carefully, both for employees still building toward it and for those weighing the right moment to take it. The 1.7% is the headline. The optionality is the real story.

William Carrington, CFP®, RMA®, is the founder of Carrington Financial Planning LLC, a virtual fee-only firm serving U.S. Foreign Service families and other federal employees.