Understanding FERS Pension Options for Eligible Family Members

For Foreign Service families, retirement planning typically focuses on the principal employee's benefits — the FSPS pension, the annuity supplement, TSP balances. What often gets overlooked is a separate federal benefit that many spouses have been quietly accumulating for years: a FERS pension earned through work as an Eligible Family Member (EFM) at post.

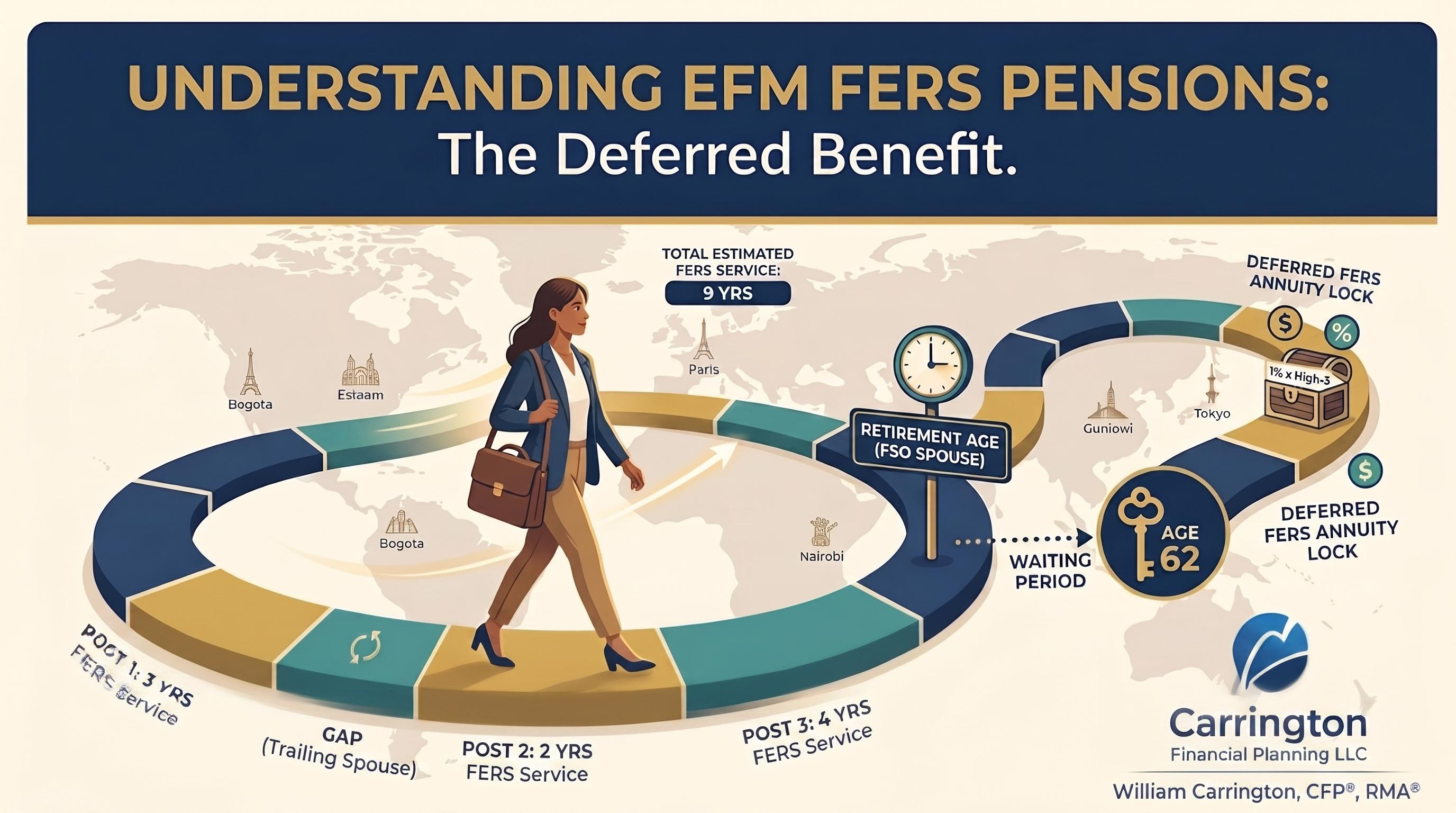

An Eligible Family Member is a spouse or other qualifying dependent who is authorized to work at a US diplomatic mission abroad. EFMs can hold a range of positions at embassies and consulates — administrative, consular, security support, and others — and when they do, they typically earn federal benefits under FERS, the Federal Employees Retirement System. By the time the principal employee retires, many EFM spouses have accumulated 10 to 15 years of FERS service across multiple postings, often without a clear picture of what that service is worth or what decisions need to be made when they separate.

Understanding those options — and the important distinctions between them — is one of the most frequently overlooked planning conversations in a Foreign Service household.

The system EFMs are actually in

A common misconception: that EFMs employed at post fall under FSPS, the Foreign Service Pension System, the same as the principal employee. They do not. EFMs are almost always covered under FERS — the same system that applies to federal civil service employees broadly. FSPS is reserved for Foreign Service employees serving in designated Foreign Service positions.

This distinction matters because FERS and FSPS have meaningfully different formulas, eligibility ages, and benefit structures. An EFM with 14 years of FERS service does not retire under FSPS rules when the principal employee retires; their benefit is calculated under FERS, on the FERS schedule, with FERS eligibility ages.

The FERS pension formula

The FERS pension is:

High-3 average salary × Years of creditable service × Multiplier

The multiplier is 1.0% for most FERS employees. It increases to 1.1% only if you separate at age 62 or later with at least 20 years of service — a threshold nearly impossible to reach through an EFM-at-post career path.

A simple example: an EFM with 12 years of FERS service and a high-3 average salary of $70,000 would have a deferred annuity calculated as $70,000 × 12 × 0.010 = $8,400 per year. Not a transformative benefit in isolation, but meaningful when it runs for life starting at age 62 — particularly alongside a full FSPS annuity from the principal employee.

Three paths: immediate, postponed, and deferred

This is where most EFMs and their financial advisors get confused, because "deferred retirement" is not the only option for someone who leaves federal service before reaching full retirement age. There are three distinct paths, and the differences matter.

Immediate retirement (MRA+10): If an EFM has reached their Minimum Retirement Age (MRA, currently 57 for most federal employees) and has at least 10 years of creditable service, they can take an immediate annuity. The downside: the annuity is reduced by 5% for each year the EFM is under age 62 at the time they begin receiving it.

Postponed retirement (MRA+10, annuity delayed): An EFM who qualifies for MRA+10 but wants to avoid the age reduction can separate from service and postpone the start of their annuity until age 62 (or age 60 with 20+ years of service). This eliminates or reduces the age penalty with no other tradeoff on the pension itself.

Deferred retirement: An EFM who separates from federal service before reaching MRA — or who reaches MRA but doesn't yet have 10 years of service — can preserve their FERS pension as a deferred annuity, payable starting at age 62 (with 5+ years of service). No age reduction applies at 62. This is the most common scenario for EFMs at post, since many separate well before reaching MRA.

Most EFMs in Foreign Service households end up in deferred retirement by default — they separate when the principal employee retires, often in their 40s or early 50s, before reaching MRA. Understanding the distinction from postponed retirement is important because an EFM who is close to MRA at separation has a meaningful choice to make.

The refund alternative — and why it's usually the wrong choice

When separating from federal service, OPM gives departing employees a choice: leave their contributions in the retirement system and eventually collect the deferred annuity, or take a cash refund of their contributions now and forfeit the pension permanently.

For most EFMs, the refund is the wrong choice. Here's why:

The refund returns only the employee's own contributions — not the government's matching share, not any investment growth. FERS employee contribution rates vary by hire date: employees hired before 2013 contributed 0.8% of salary; employees hired in 2013 contributed 3.1%; employees hired in 2014 or later contribute 4.4%. For an EFM who worked 12 years at federal salary levels, even at the higher 4.4% rate, the lump-sum refund is a modest one-time payment. The deferred annuity, by contrast, pays for life starting at 62, with cost-of-living adjustments that begin once payments start.

Taking the refund also permanently severs the federal service credit. If the EFM ever returns to federal service — at a future domestic posting, in a subsequent position, or after the principal employee's retirement — they cannot buy that service back. The continuity is gone.

The rare case where a refund might be considered: immediate financial hardship, or a clear determination that the EFM will never draw on the deferred pension. We see this almost never in practice.

A note on FEHB

For most Foreign Service households, health coverage in retirement is not a planning issue tied to the EFM's own employment record. The family carries FEHB through the principal employee's retiree coverage, with the EFM enrolled as a covered family member. Whether the EFM qualified for FEHB through their own federal service generally doesn't affect day-to-day coverage.

The picture changes in two scenarios. If the principal employee dies, survivor benefit elections and the associated FEHB continuation provisions govern coverage — a topic handled separately in the retirement planning process. Divorce is a more complicated exposure: upon divorce, the EFM loses eligibility as a family member under the principal employee's FEHB plan. While spouse equity provisions allow former spouses to continue coverage in some circumstances, this typically involves paying the full premium with no government contribution, and coverage continuity is not guaranteed. In practice, divorce can leave an EFM without affordable group health coverage — a risk worth acknowledging, even if it's not the central planning issue for an intact household.

A note on COLAs

Deferred FERS pensions are not adjusted for inflation between the date of separation and the date the pension begins. The benefit computed at separation is the benefit that begins at 62 — in nominal dollars, with no inflation protection during the waiting period. Once payments begin, COLAs apply annually. For an EFM who separates at 50 and waits 12 years to collect, the real purchasing power of the benefit at 62 will be lower than the nominal amount suggests. This is worth factoring into the household income picture.

Planning takeaways

The FERS benefit earned through EFM service is a real and often undervalued household asset. The decisions that shape it — whether to take a refund, which retirement path to elect, and whether the EFM should extend federal service to reach MRA before the principal employee retires — are worth modeling carefully before the principal employee's retirement date, not after. For EFMs approaching MRA with 10+ years of service, the postponed retirement option deserves specific attention since it eliminates the age reduction penalty.

Federal retirement rules are also under active legislative discussion. FERS contribution rates, benefit formulas, and the FERS annuity supplement for other federal employees have all been the subject of recent congressional proposals. Rules that apply today may shift; working with an advisor who tracks these changes is part of navigating them effectively.

Carrington Financial Planning is the fee-only fiduciary financial advisor for U.S. Foreign Service employees and other federal employees. We routinely model FSPS and FERS benefits together for Foreign Service households, including the deferred and postponed pension options available to EFM spouses. To discuss your household's federal benefits picture, schedule a free initial consultation.

This article is for educational purposes only and does not constitute tax, legal, or investment advice. Federal benefits rules are complex and individual circumstances vary; please consult a qualified advisor or OPM directly before making decisions based on this information.