Your Hardship Posts Won't Boost Your Pension: How the FSPS High-3 Actually Works

One of the most common — and most expensive — assumptions I see among Foreign Service employees is that the big number on an overseas paycheck is the number their pension is built on. After all, between danger pay, hardship differential, and COLA, total compensation at a tough post can run far above base salary. It feels like those years should count for more.

They don't. Your FSPS pension is built on a much narrower figure, and understanding which dollars count — and which don't — changes how you should plan.

What the high-3 actually measures

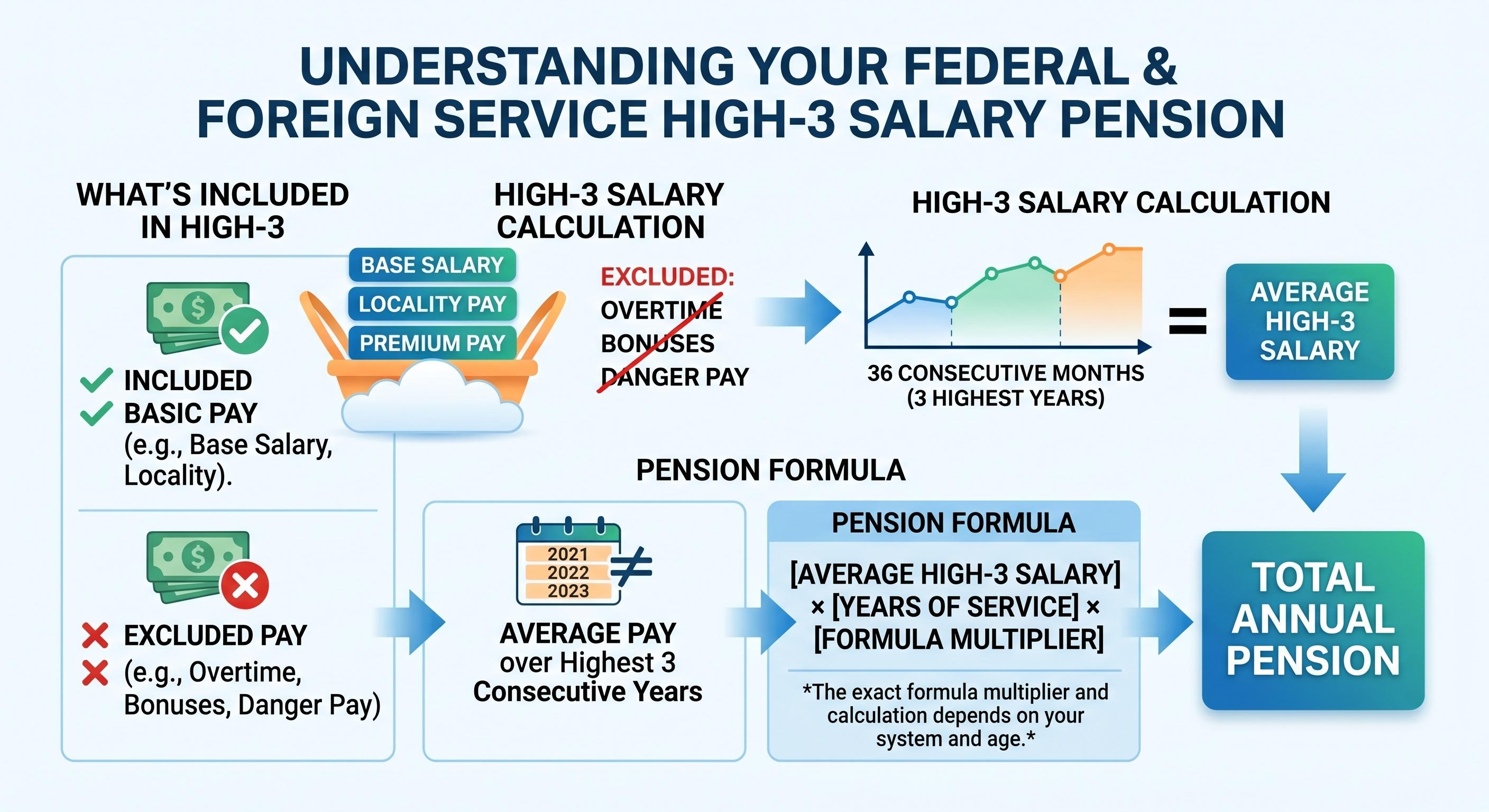

Your FSPS annuity is based on your high-3: the highest average basic pay over any 36 consecutive months of your career. A few things worth knowing:

- It doesn't have to be your last three years — it's whichever consecutive 36-month stretch was highest, wherever it falls in your career.

- It doesn't have to align to calendar years.

- That average is multiplied by 1.7% for each of your first 20 years of service, plus 1% for each year beyond 20.

So the entire calculation hinges on what the government counts as "basic pay." And that's where the misconception lives.

What counts — and what doesn't

Counts toward your high-3:

- Your salary-schedule base pay

- Domestic locality pay (when assigned in the U.S.)

- Overseas Comparability Pay (OCP) — the "virtual locality pay," set at 22.62% of base in 2026. OCP counts because it's treated as locality pay.

Does not count:

- Danger pay

- Post (hardship) differential

- Cost-of-living allowance (COLA)

- Post allowance and other foreign-area allowances

- Overtime (which never counts toward anyone's high-3)

That second list can make up a large share of what hits your bank account overseas. None of it feeds your pension.

A quick example

Imagine an employee spending their highest-earning years at a 35% danger-and-hardship post. Their total compensation might look impressive — base, plus OCP, plus a danger differential, plus hardship, plus COLA and post allowance. But when it comes time to compute the pension, only base pay and OCP go into the high-3. If those total an average of, say, $140,000 across the three best consecutive years, then $140,000 is the high-3 — not the inflated total that showed up on the pay statements.

At 25 years of service, that's roughly 28.5% of $140,000 — about $39,900 a year — regardless of how much danger pay padded the paychecks along the way.

Why this matters for your planning

Employees who spend their peak years at hardship posts routinely overestimate their pension, because they anchor to total compensation rather than to base-plus-OCP. The fix is simple: plan from the real high-3, not the paycheck.

It also reframes the role of your TSP. The FSPS pension plus Social Security was never designed to replace your full pre-retirement income — and the allowances that boosted your overseas earnings don't carry into the pension at all. That puts more weight on the TSP to close the gap. And because the Foreign Service has mandatory retirement at 65, your accumulation window is finite in a way most federal employees' isn't. The earlier you treat the TSP as the workhorse rather than the supplement, the better that math works out.

If you're targeting a retirement date, it's worth confirming your actual high-3 — based on your specific assignment history and how each was classified — rather than estimating from memory of what your paychecks looked like.

Carrington Financial Planning is a fee-only fiduciary firm that primarily serves Foreign Service and federal employees. This post is educational and not individualized financial advice; your actual high-3 depends on your service history, so confirm the figure before building a retirement date around it.