Roth In-Plan Conversions Come to the TSP — and Most Foreign Service Employees Should Wait

As of January 28, 2026, the Thrift Savings Plan offers something it never has before: the ability to convert money from your traditional (pre-tax) TSP balance to your Roth (after-tax) balance without leaving the plan. Historically, federal employees who wanted this strategy had to roll money out of the TSP into a private IRA to do it — giving up the TSP’s rock-bottom costs in the process. Now you can run the same play inside the plan.

It’s a genuinely useful tool. It’s also one of the easier ways to make an expensive mistake if you reach for it at the wrong time. Here’s how it works, when it actually pays off, and the one prerequisite that decides whether a conversion makes sense at all.

What actually changed

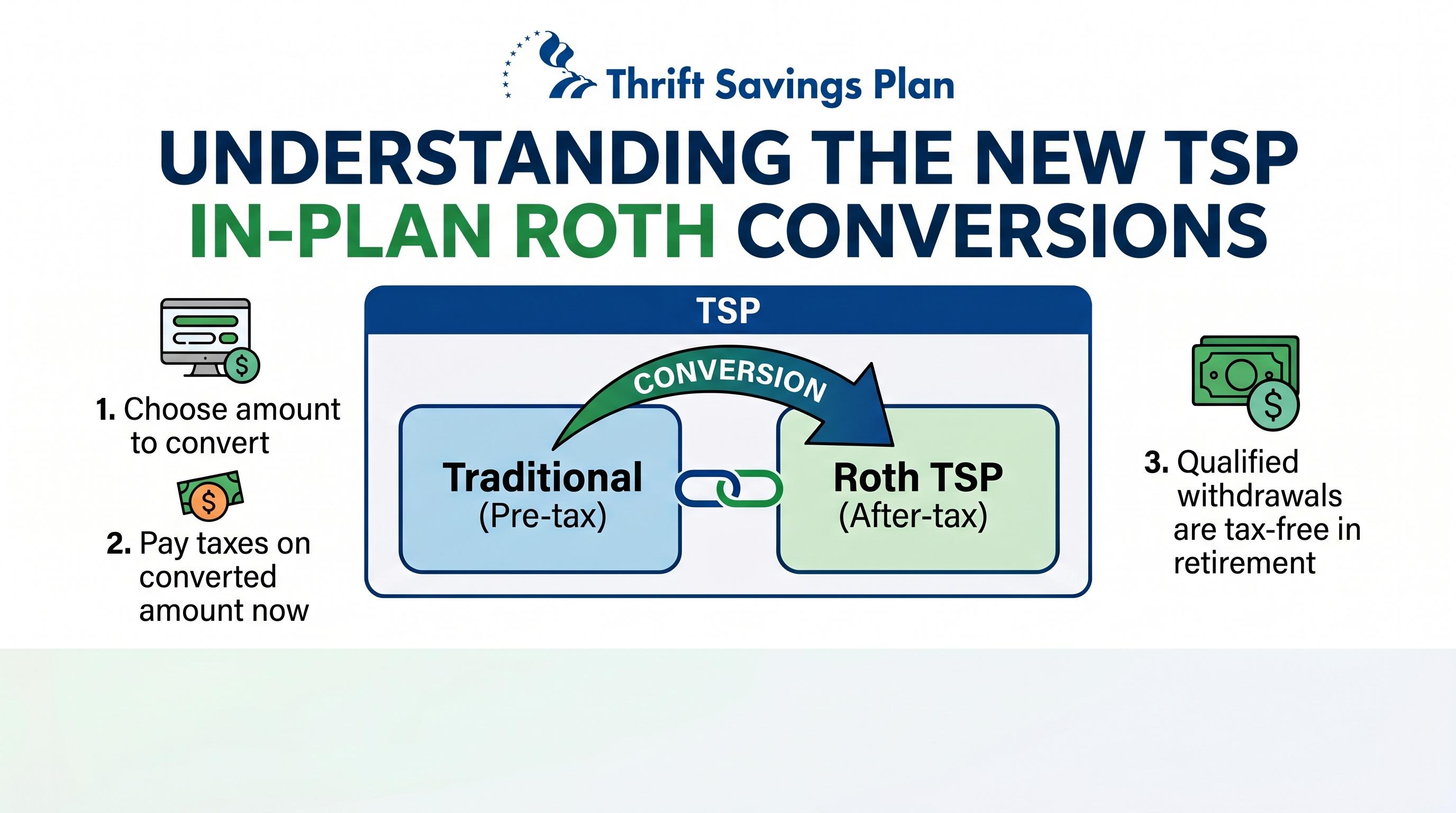

A Roth in-plan conversion moves dollars from your traditional TSP into your Roth TSP. You don’t roll anything out of the plan, and you don’t need to separate from service. You log into My Account, choose an amount — a flat dollar figure or a percentage — and the conversion happens inside your existing TSP.

A few mechanics worth knowing:

- You can request up to 26 conversions per account per year, so you’re not locked into a single all-or-nothing move.

- You need at least $500 in vested funds to convert.

- The converted amount becomes taxable income in the year you convert it, taxed at your ordinary marginal rate. You’ll see it on a 1099-R the following January.

- Conversions don’t count against your annual contribution limit, so converting doesn’t reduce how much you can keep contributing.

- A conversion is irrevocable once processed. There’s no recharacterization, no undo.

That last point is the one to sit with. Unlike a contribution decision you can adjust next pay period, a conversion is permanent the moment it clears.

The whole game is timing: find your “Tax Valley”

The entire value of a Roth conversion comes from one comparison: the tax rate you pay now on the converted dollars versus the rate you’d pay later when you’d otherwise withdraw them. Convert at a lower rate than your future rate and you win. Convert at a higher rate and you’ve simply prepaid taxes for no benefit — and you’ve done it with money you can’t get back.

So the goal is to convert during a “Tax Valley” — a stretch when your taxable income is temporarily lower than usual, and your marginal rate dips with it.

For most people, that valley arrives after retirement: you’ve stopped drawing a salary, but you haven’t yet claimed Social Security and you’re not yet forced to take required minimum distributions (which begin at 73). Income falls, the bracket falls, and that gap is the natural runway for conversions. This is exactly why converting while you’re still working is usually a mistake — your career years are at or near your lifetime peak income, with locality or overseas comparability pay stacked on top of base salary. A conversion in a high-earning year piles taxable income on income that’s already high and means paying the most you’ll ever pay to move the money.

For Foreign Service families, the valley sometimes comes early

Here’s the wrinkle that makes this different for the Foreign Service: the Tax Valley doesn’t always wait until retirement. The FS lifestyle can open one while you’re still an active employee. Two situations are worth watching for.

An EFM spouse between jobs. If your household has been running on two incomes and your eligible family member is between positions — common given the constant moves of FS life — your taxable household income can drop sharply for a year or two. That dip is a valley.

Allowance-heavy overseas years. Much of what funds your life at post — COLA, housing, and other allowances — isn’t taxable income, and (as I’ve written elsewhere) it doesn’t even count toward your high-3. So during a posting where allowances carry a large share of your standard of living, your taxable gross can sit well below how comfortable your life actually feels. Low taxable income is, again, a valley — even though your total compensation looks high on paper.

In either case, a year of artificially low taxable income is a year you might convert traditional TSP dollars to Roth and lock in a rate you won’t see again once you rotate back stateside or your household income recovers. (The opposite case exists too: a high earner with a large pension who stays in a top bracket straight through retirement may never get a deep valley, and for them converting earlier rather than later can make sense.)

The point isn’t that conversions are bad. It’s that converting on autopilot during a high-income year destroys the benefit — and the skill is recognizing your valleys, wherever in your career they fall.

You need money outside the TSP to pay the tax

Here’s the prerequisite that quietly decides most cases.

When you convert, you owe ordinary income tax on the full converted amount. And with an in-plan conversion, you cannot have that tax withheld from the conversion itself — the entire amount you convert stays in the plan and becomes Roth. No dollars come out to cover the IRS.

So the tax has to be paid from somewhere else: a taxable brokerage account, savings, or other non-TSP funds. If the only way you can cover the tax bill is by pulling money out of the TSP, you’ve undercut the whole strategy. You’d generate even more taxable income to raise the cash, you might trigger an early-withdrawal penalty if you’re under 59½, and you’d shrink the balance that gets the tax-free Roth treatment in the first place.

A clean rule of thumb: if you can’t write the tax check from outside the TSP, you’re not ready to convert.

The payoff: tax-free growth, no RMDs, and a cleaner legacy

Done in the right year, the upside is real and lasting. Roth TSP dollars grow tax-free and come out tax-free in qualified retirement, and — as I covered in an earlier post — Roth TSP balances are no longer subject to lifetime required minimum distributions under SECURE 2.0. Unlike your traditional balance, the government can’t force you to start drawing your Roth down at 73.

That last point matters more than it first appears. For many Foreign Service retirees, the FSPS pension and Social Security cover day-to-day living expenses — which means the TSP can become a legacy asset rather than a spending account. A Roth balance passes to your heirs income-tax-free; a traditional balance passes them a tax bill. Converting in a low-bracket year — your valley — is how you move money from the taxable column to the tax-free one at the lowest possible cost.

That’s a meaningful long-term advantage. It just isn’t a reason to rush.

Bottom line

This is a planning decision, not a button to push — and it’s irreversible once done. The work is identifying your Tax Valley (which, for Foreign Service families, may arrive years before retirement), confirming you can pay the tax from outside the TSP, and sizing the conversion to fill out the low bracket without spilling into a higher one. That’s worth modeling against your actual pension, income timeline, and bracket projections rather than guessing — ideally before the valley arrives, so you’re ready to act when it does.

Carrington Financial Planning is a fee-only fiduciary firm that primarily serves Foreign Service and federal employees. This post is educational and not individualized tax or investment advice.