State Income Tax and the Foreign Service: Your Domicile Is a Decision, Not an Accident

You can spend three years at post without setting foot in your “home” state — and that state may still tax every dollar of your federal salary. Or it may tax none of it. The difference comes down to one concept that most Foreign Service employees drift into rather than choose: domicile.

Getting it right is worth real money over a career. Getting it wrong — or never deciding at all — can quietly cost you thousands a year for decades.

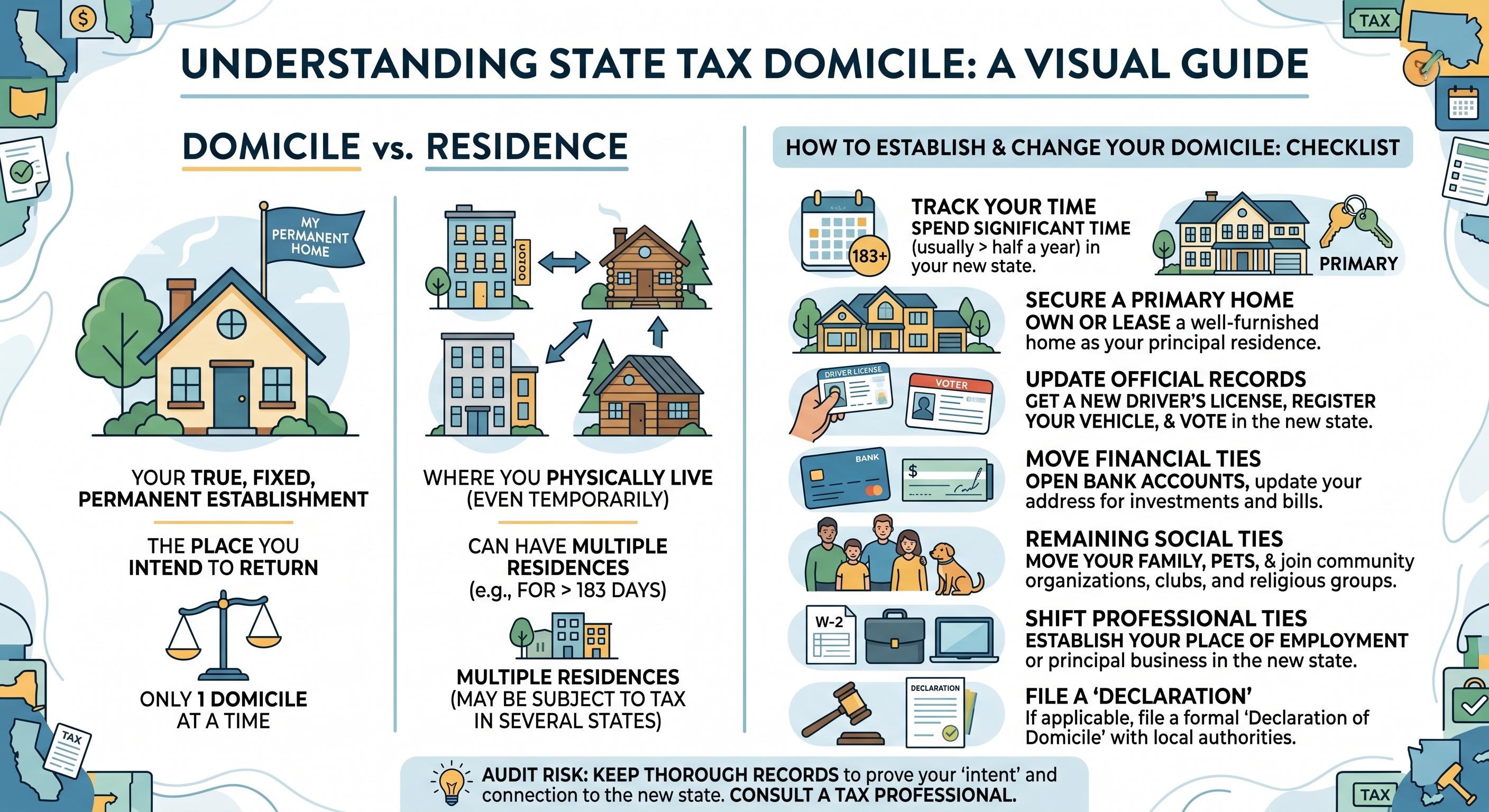

Domicile is not the same as where you live

Federally, you’re taxed on your worldwide income no matter where you’re posted; an overseas assignment doesn’t change that. State income tax is different. It turns almost entirely on domicile — your one true, permanent legal home, the place you intend to return to. You keep your domicile until you deliberately establish a new one somewhere else. Being physically absent for years, even on the other side of the world, doesn’t change it by itself.

So the question isn’t “where do I live?” — for a Foreign Service employee that answer changes every couple of years. The question is “which state is my legal home, and is that the state I want it to be?”

If your domicile is a no-income-tax state — Florida, Texas, Washington, Tennessee, Nevada, and a handful of others — your federal salary generally escapes state income tax entirely while you serve. If your domicile is a high-tax state like California, Virginia, or New York, that state can tax your full federal salary even while you’re sitting at a desk overseas.

The catch that’s specific to the Foreign Service

Here’s the part that trips people up: you don’t get the protections military members do.

Service members and their spouses have the Servicemembers Civil Relief Act and the Military Spouses Residency Relief Act, which let them lock in a state of legal residence and keep it regardless of where orders send them. There is no equivalent statute for Foreign Service civilian employees. Your domicile is governed by ordinary state law and by the facts of your own life — which cuts both ways. You have more freedom to choose, and less protection if you choose carelessly.

States don’t decide domicile by any single factor. They look at the whole picture: where you’re registered to vote, where your driver’s license and vehicle are registered, where you own or rent property, where your bank and financial accounts sit, where your family is, where you file resident tax returns, and your demonstrated intent to return. For Foreign Service employees, the analysis often centers on the state you joined the Service from, your home-leave address, or the state you genuinely plan to return to upon separation.

The “sticky state” trap

If you entered the Service domiciled in a high-tax state and never affirmatively changed it, that state can keep claiming you for as long as the facts point its way. Some states make leaving genuinely difficult — they expect you to sever your connections and clearly demonstrate you’ve abandoned the old domicile and established a new one. A driver’s license you never updated, a house you kept, a voter registration you forgot about — any of these can give an aggressive state a reason to keep taxing you.

The flip side is the opportunity. Many Foreign Service employees legitimately establish domicile in a no-tax state, usually around a real-life anchor: a CONUS assignment, a home purchase, a family relocation. The key is consistency. Domicile has to reflect genuine ties and genuine intent — you can choose where to plant them, but you can’t fake them. Half-measures (claiming Florida while keeping a California license, a California home, and California voter registration) invite a challenge you’ll probably lose.

One practical note: the “state of legal residence” you have on file with the Department drives your state tax withholding, but it doesn’t by itself establish domicile. The underlying facts do. If your stated residence and your actual life don’t line up, fix the facts — don’t just change the form.

Bottom line

This isn’t a do-it-yourself project, especially if you’re trying to leave an aggressive high-tax state. State rules vary enormously, and a sloppy change can leave you exposed to two states at once. But it’s also one of the few planning levers in a Foreign Service career that can pay off every single year — so it’s worth being intentional about, ideally before a move rather than after.

If you’re not sure which state currently considers you its own, that’s the first thing worth pinning down.

Carrington Financial Planning is a fee-only fiduciary firm that primarily serves Foreign Service and federal employees. This post is educational and not individualized tax or legal advice; state domicile rules vary, so confirm your situation with a qualified professional before acting.