The Golden Handcuffs of the FSPS: What Leaving the Foreign Service Early Really Costs

By William Carrington, CFP®, RMA®

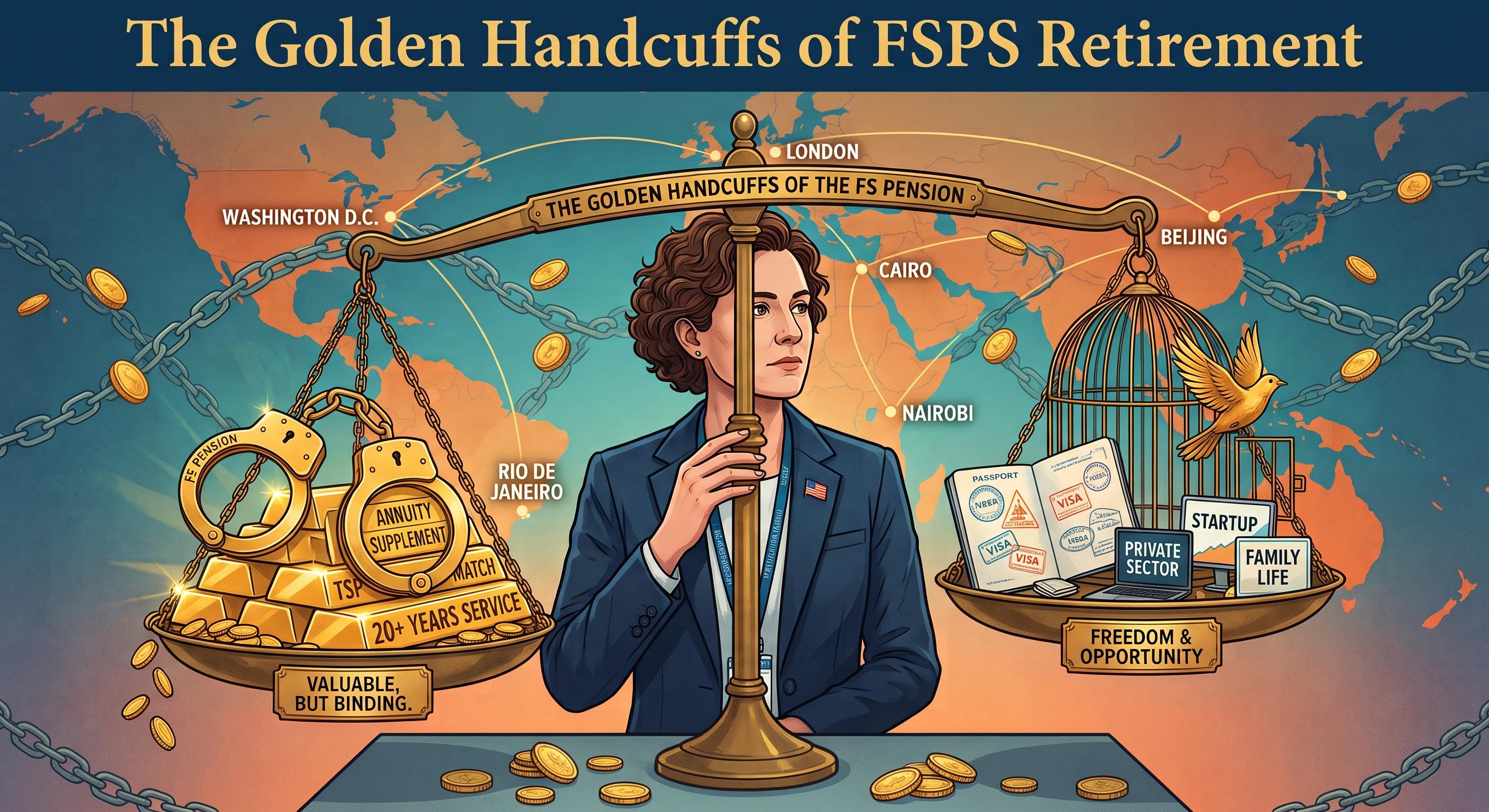

If you're a mid-career Foreign Service officer, there's a decent chance you've run the thought experiment recently: what would it actually cost me to leave? Maybe it's a private-sector offer, a spouse's career, family needs, or simply the turbulence at the Department over the past year and a half. Whatever the trigger, the question deserves a real answer — not a gut feeling. And the honest answer is that the FSPS pension is built with golden handcuffs, and they're tighter than most officers realize.

What you keep by staying

Retire on an immediate annuity — for most officers, that means age 50 with 20 years of service — and the FSPS treats you generously. Your annuity is computed at 1.7% of your high-three average salary for each of your first 20 years (1% for years beyond 20). You receive the annuity supplement, a bridge payment approximating your Social Security benefit, from retirement until age 62. You carry your FEHB health insurance into retirement for life, with the government still paying roughly 70% of the premium. And your annuity receives cost-of-living adjustments from the start.

Every one of those benefits is conditioned on reaching immediate-annuity eligibility. Walk out the door early, and they don't shrink proportionally — most of them vanish.

What actually happens if you leave early

Resign before you're eligible for an immediate annuity, and your only pension option (assuming you leave your contributions in the fund) is a deferred annuity, generally beginning at age 62. Here's what that deferral really costs:

The enhanced multiplier disappears. A deferred FSPS annuity is calculated at 1% per year of service — for all years. The 1.7% rate is reserved for those who retire on an immediate annuity. This surprises even well-informed officers, and some older publications still get it wrong. Leave at 15 years and your multiplier isn't 'reduced' — it was never yours to begin with.

Your high-three is frozen in time. The salary average used to compute a deferred annuity is your high-three at separation, with no inflation adjustment during the waiting years. Separate at 45 and the annuity you start collecting at 62 is based on a salary figure that's had seventeen years of purchasing power quietly eroded out of it.

No annuity supplement. The bridge payment is only paid to those retiring on an immediate annuity.

No retiree health insurance. This may be the biggest one. FEHB in retirement requires retiring on an immediate annuity. Resign early and you cannot restart FEHB later — you're buying private health insurance from your departure until Medicare, and paying full freight for supplemental coverage after. FEGLI life insurance terminates as well.

A worked example

Consider an officer, age 45, with 15 years of creditable service and a high-three of $180,000. She's weighing a private-sector offer against staying five more years to reach 50/20.

If she leaves now: her deferred annuity at 62 is 1% × 15 years × $180,000 — $27,000 per year, starting seventeen years from now, in frozen dollars. At 2.5% inflation, that $27,000 will have the purchasing power of roughly $17,700 today. No supplement, no FEHB, no COLAs until the annuity begins.

If she stays to 50/20: assume modest raises bring her high-three to $195,000. Her immediate annuity is 1.7% × 20 × $195,000 — $66,300 per year, starting at age 50, with COLAs. Add an annuity supplement of roughly $12,000 per year until 62, and lifetime retiree FEHB with the government paying the lion's share of premiums.

Just the twelve years between 50 and 62 — annuity plus supplement — total roughly $940,000 before any COLAs. After 62, the gap continues: about $66,000 (COLA-adjusted) versus $27,000 in shrunken dollars, every year, for life. Layer in the retiree FEHB subsidy, plausibly worth $10,000 or more per year for a couple, and the lifetime value forfeited by leaving at year 15 comfortably exceeds $1.5 million.

Put differently: those final five years of service carry roughly $300,000 per year in retirement value on top of her salary. That's the number the private-sector offer has to compete with — not just her current pay.

What isn't handcuffed

It's worth being precise about what you do keep. Your TSP is fully portable — your balance, including agency contributions if you're vested, goes with you, and it keeps growing wherever you leave it. Your Social Security earnings record continues building in private employment. And your retirement contributions can either stay in the fund (preserving the deferred annuity) or be refunded — though taking the refund permanently extinguishes your pension rights, which is rarely the right move for anyone with meaningful service.

When leaving early still makes sense

None of this is an argument that no one should ever leave. A private offer large enough to clear that break-even — and they exist, particularly for officers with specialized skills — changes the math entirely. So can a spouse's career, your health, your family's needs, or the simple fact that a career you've come to dread is a poor trade for any pension. Involuntary separations follow different and somewhat more forgiving rules, which is a topic for another post.

The point is narrower: make the decision with the real numbers in front of you. The FSPS is deliberately back-loaded, and the difference between year 15 and year 20 is not five-twentieths of a pension — it's most of the pension. If you're weighing an exit, run the analysis first. It's precisely the kind of question a comprehensive financial plan is built to answer.

This post is for educational purposes only and is not individualized advice. Figures are illustrative; your own eligibility, service history, and benefit calculations should be verified against your official records before making any separation decision.