The TSP Tax Trap at the Second Passing

The Thrift Savings Plan handles the first death in a family gracefully. It handles the second one brutally. This is a rule almost no federal family knows about — including many who have spent entire careers around federal benefits — because it never surfaces during the employee’s life, and not even at the employee’s death. It surfaces years later, when the surviving spouse dies, and by then the family it hurts is rarely talking to anyone who saw it coming.

At The First Passing

Meet a typical Foreign Service family. Daniel spent a career in the Foreign Service and retired with $800,000 in his TSP. His wife, Ana, accompanied him from post to post; their two children are grown. When Daniel dies, Ana — his designated beneficiary — keeps the money right where it is. The TSP opens an account in Ana’s name, and Daniel’s balance moves into it.

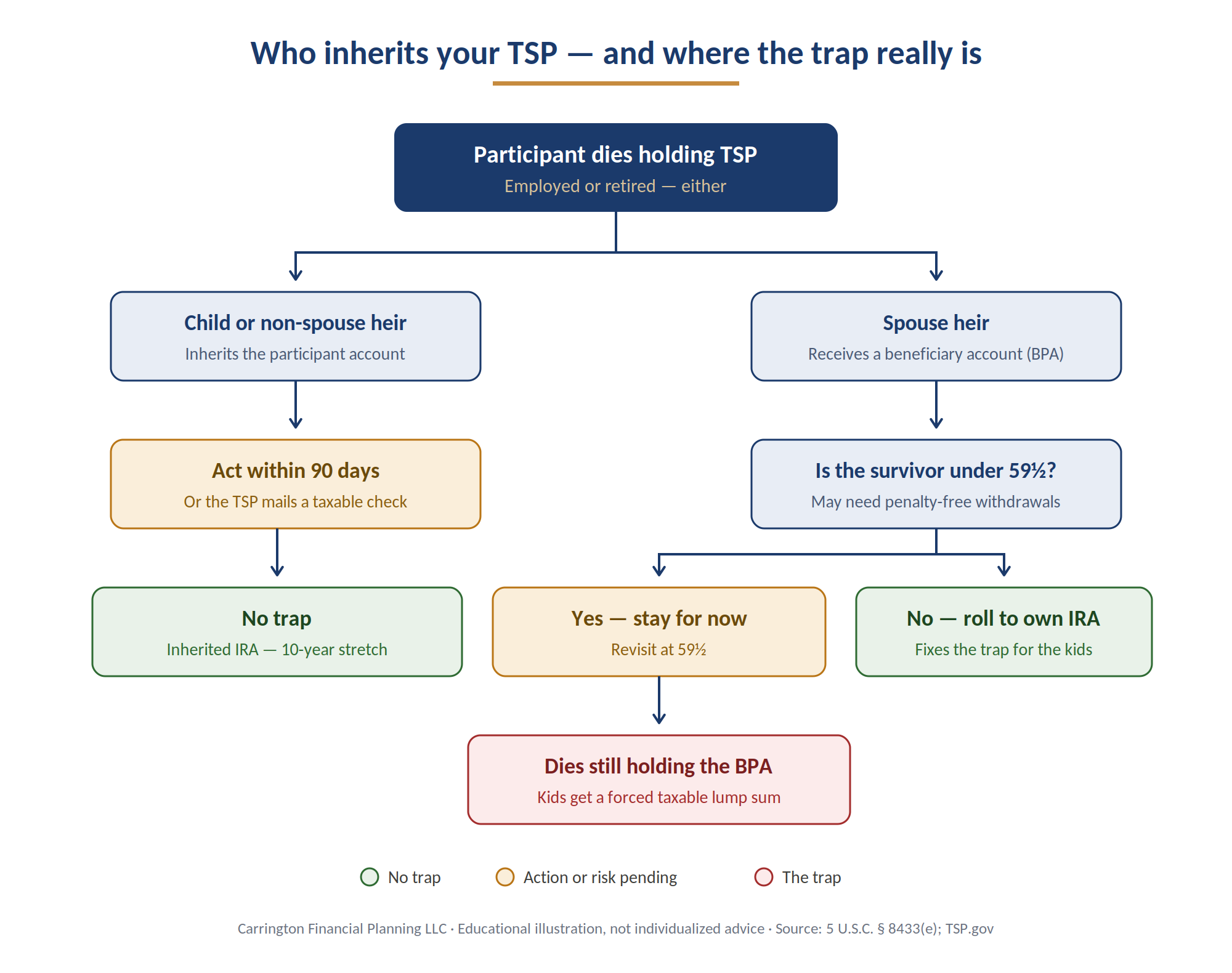

The chart below maps the whole decision. Two details deserve emphasis before you read it. First, this rule applies to every TSP participant — active federal employees and retirees alike, across every agency, not just the Foreign Service. Second, notice that both paths require a survivor to act. A child inheriting directly from a participant's account has just 90 days to direct the funds into an inherited IRA; miss that window and the TSP simply mails a taxable check. A surviving spouse holding a beneficiary account has no deadline at all — which is precisely why the rollover gets postponed indefinitely, until a second death makes the outcome permanent.

If you take one thing from this chart, take this: the trap lives in only one place — a beneficiary participant account still open at the survivor's death. Everything else on the map has a clean exit, provided someone knows to use it.

Here is the detail that matters, and that nothing on Ana’s statements will ever announce: the account Ana now holds is not a regular TSP account. It is a beneficiary participant account, or BPA — a legally different kind of account with different inheritance rules. To Ana it looks identical: same TSP website, same G and C Funds, same low costs, and flexible withdrawals with no early-withdrawal penalty at any age. Everyone in the family now thinks of it as “Mom’s TSP.” That is precisely the problem. It is not Daniel’s TSP anymore, and it is not a normal TSP either — and the difference will not matter for years, until suddenly it is the only thing that matters.At The Second Passing: The Trap Springs

Years later, Ana dies, and the children inherit. This is the moment the BPA reveals what it is. The rules for the next generation are set by statute, and they are exceptionally rigid: the children cannot keep the account in the TSP, and a death benefit paid from a BPA cannot be rolled over into any IRA or retirement plan. The inherited IRA that would normally let heirs spread withdrawals over ten years under the SECURE Act is explicitly off the table. The TSP has no choice but to pay out the entire remaining balance as a single cash distribution.

For traditional pre-tax balances, the consequence is severe. Each of Daniel and Ana’s children receives $400,000 of ordinary income in a single tax year, stacked on top of their salaries. Most of it lands in the 32–35% federal brackets or higher, before state tax — easily $130,000 or more in tax per child. Had the same money arrived in an inherited IRA, each child could have drawn it down across ten years, keeping most withdrawals in far lower brackets. The difference is often a six-figure sum the family never needed to lose.

Be clear about which account is the culprit, because this is where families get confused. If the children had inherited directly from Daniel — if Ana had died first, or if Daniel had named the children as beneficiaries on his own account — they would have had 90 days to move their shares into inherited IRAs, and the ten-year option would have been theirs. The trap is not Daniel’s TSP. The trap is what Daniel’s TSP quietly became in Ana’s hands. Same children, same money, opposite outcomes — decided entirely by whether the money was still in a participant’s account or had become a BPA.

The Fix: One Rollover

The escape is simple, and it is entirely in Ana’s hands: do not treat the BPA as a permanent vault. A spouse beneficiary has the right, at any time, to roll the BPA into their own IRA — traditional balance to a traditional IRA, Roth balance to a Roth IRA. That single transfer strips away the TSP’s restrictive successor rules; the money simply becomes Ana’s own retirement asset. When she eventually passes, the children inherit an ordinary IRA, open inherited IRAs of their own, and manage the taxes deliberately across the SECURE Act’s ten-year window.

Timing matters, and the BPA’s advantages are real — there is no need to rush. A survivor under 59½ who needs the money should generally stay in the BPA, because the penalty-free access disappears once the funds move to an IRA. But once that need has passed — the survivor reaches 59½, or simply doesn’t need withdrawals — the rollover should move to the top of the list. And if the surviving spouse is a federal employee or retiree in their own right, there is a second cure: combining the BPA into their own TSP account, which likewise restores normal beneficiary treatment for the children.

What To Do With This

If you are a federal employee or annuitant: make sure your spouse knows this rule exists, because the fix will one day be theirs to execute. Put a note with your estate documents. If your household already includes a widow or widower holding a BPA — a parent, perhaps — this deserves a conversation now, while the fix is still available. And whatever your situation, confirm your TSP beneficiary designation is current; the TSP pays by the designation on file, not by your will.

The TSP is one of the best retirement vehicles in America, and for the surviving spouse it remains a fine temporary home. It just makes a poor inheritance vehicle for the generation after that. One rollover, executed at the right time, is all it takes to keep a lifetime of disciplined saving from ending in a single avoidable tax bill.

This article is for educational purposes only and does not constitute individualized financial, tax, or legal advice. The family described is fictional and tax figures are illustrative. Federal benefit and tax rules change; verify current provisions with the TSP and IRS, or consult a qualified advisor regarding your specific situation.